Life is full of surprises, but a financial one triggers you immediately. It makes you panic at the hour of need. Not having cash when you need it most impacts mental peace. It leads to rather severe consequences. You may need to buy that medicine urgently or treat the blocked backsplash. An emergency can find you in any shape and at any time.

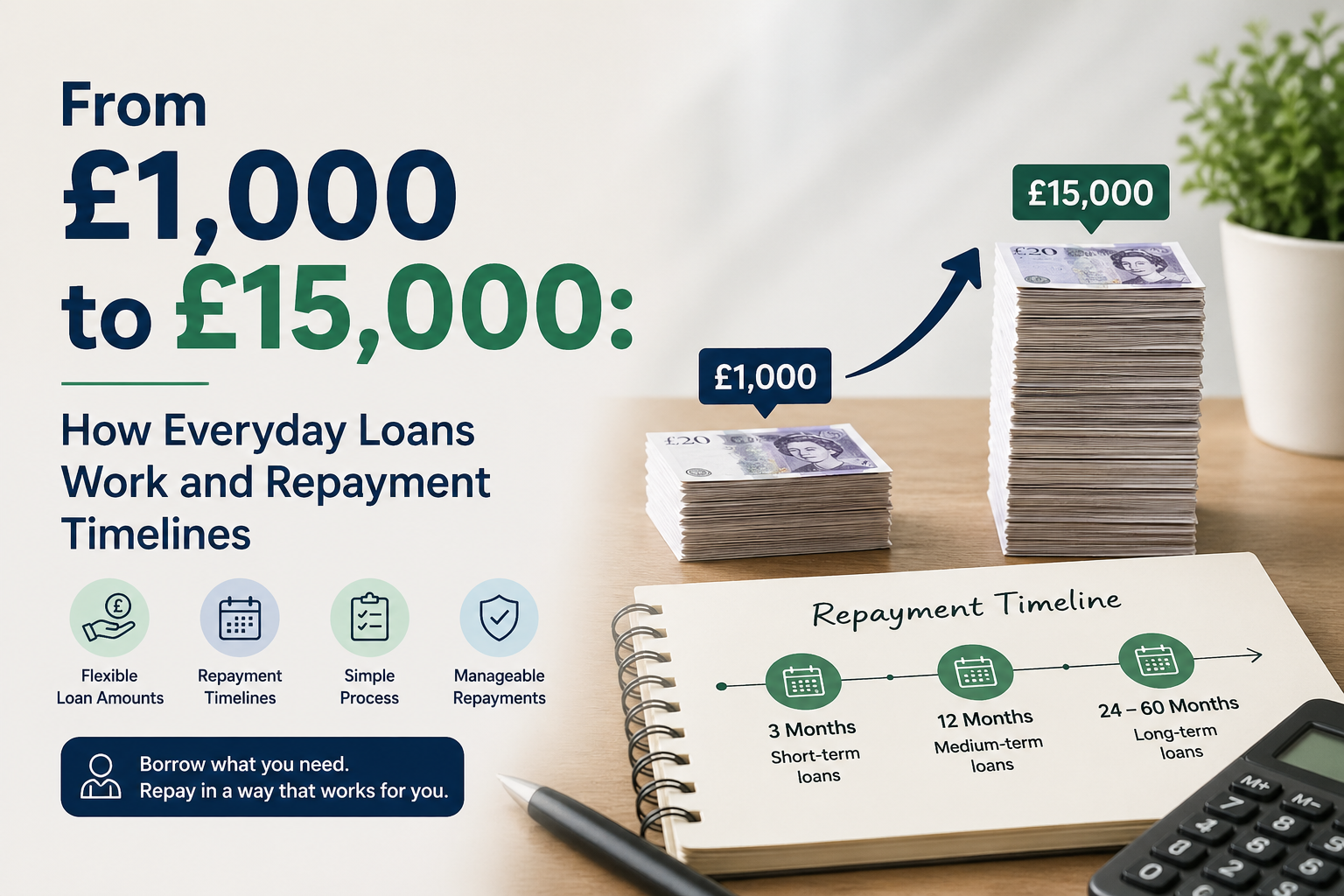

Therefore, everyday loans may immediately calm your anxieties. You may get £1000-£15000 for any business or personal cash needs. These loans are mostly unsecured. Thus, it gives you better control over your assets and helps you meet needs without worries. The blog discusses how everyday loans work and what repayment timelines you may expect.

What do you mean by everyday loans?

Everyday loans, as the name suggests, are a financial facility one can tap for any regular needs. It may help with bridging rent payments, clearing utility bills, or attending medical emergencies. The approval of these loans is mainly based on income rather than credit scores. Individuals with bad credit history may also qualify if they can afford the loan payments.

These loans are unsecured in nature. It means one can get £1000-£15000 even as a student, self-employed, or unemployed (with a part-time income). The amount depends on your needs and affordability. It is the reason the interest rates on these loans are slightly higher than those on secured loans.

Still, the ability to repay a fixed amount every month releases the worries. Instead, one can easily budget and repay as per the loan agreement. The repayment terms are 1-5 years. One can repay according to income, monthly expenses, and other life goals.

What criteria do you need to match to get everyday loans from direct lenders?

Getting everyday loans from direct lenders in the UK requires you to meet specific criteria. It may differ slightly according to the loan providers. Here is the basic one that you may encounter:

- Citizenship and age

You generally need to be 18+ as a permanent UK citizen to qualify for the loan. In some cases, individuals on a visa may also qualify. However, the amount may remain less in that case.

- No need for home ownership

Individuals do not need to be homeowners to qualify for the loan. Individuals who are renting spaces and students living in specific hostels and accommodations may qualify.

- Reliable income and bank account

One must hold a verified income as a full-time/part-time/ self-employed worker. On average, one should earn £10000/year to qualify for the loans. Unemployed receiving benefits may also qualify if they have a part-time or secondary income source from a reliable source.

Alternatively, individuals must hold a country-specific bank account, preferably with a direct debit facility. It helps individuals with limited credit history and bad credit qualify quickly.

- Must have a permanent residential address

An inconsistent or unstable residential address reveals unreliability on the borrower’s part. Instead, individuals with a lengthy and stable residential history of at least 6 months at a place may qualify.

How does Everyday Loans work in the UK?

Imagine a loan that counts your present and does not judge your past. Yes, it does exist. Everyday loan focuses on your current income and affordability. You do not face rejection for past mistakes, missed payments, or a CCJ. Precisely, you never miss a chance to improve past doings alongside meeting your needs. Here is how everyday loans work in the UK:

- Step 1- Begin with a simple application

Identify the amount you need (from £1000 to £15000) for your specific purpose. Determine how much you have in savings and decide the amount to borrow accordingly. Fill a simple loan application by mentioning details like name, email ID, contact details, purpose of the loan, and bank account number. Analyse the symbols, characters, and spellings before clicking “apply”.

- Step 2- Get a quick “soft” quote

Once you apply, the loan company receives and provides a quick quote within 60 seconds or a minute. Response times may vary according to the specific loan company’s process. This quote lists the approximate terms (loan amount, interest, monthly repayments, and total repayable amount).

It gives you a peek into what your agreement may look like. However, it is not the final quote. It just helps you analyse the approximate amount without affecting the credit score.

- Step 3- Provide a few documents

The best part about these everyday loans is the limited documentation. Moreover, the OpenBanking technology makes it easier for loan companies to analyse affordability. What could be better than getting a loan without the hassle of uploading documents? It thus cuts turnaround times and helps you counter needs quickly. Here are the documents that you may need to provide:

| 📄 Document | 🎯 Why Lenders Need It | ✅ How It Improves Approval Chances |

| Proof of Identity (Passport/Driving License) | Confirms your identity and prevents fraud | Shows legitimacy and speeds up verification |

| Proof of Address (Utility Bill, Council Tax) | Verifies UK residency and stability | Demonstrates reliability and fixed residence |

| Proof of Income (Pay slips, Bank Statements) | Assesses your ability to repay the loan | Strong income evidence increases trust and the potential for loan size |

| Bank Statements | Reviews spending habits and financial health | Shows responsible money management |

| Employment Details | Confirms job stability and regular income | Stable employment reduces perceived risk |

| Right to Reside (Visa/Status if applicable) | Confirms legal right to live in the UK | Ensures eligibility and long-term repayment capability |

- Step 4- Get the final quote

Loan companies crunch your income vs. outgoings. It helps them analyse whether you meet the basic criteria like (10k/year earnings, UK bank account, age over 18), etc. If your expenses are low and your income exceeds the amount required, you may qualify. The best direct lenders in the UK may design a personalised quote that meets your needs and is affordable. It thus helps you get debt-free without affecting other goals.

- Step 5- Check and Decide the repayments

Usually, you get the freedom to choose the repayment term at the time of loan application or after you submit the documents. Choosing a longer repayment term implies paying more interest. Similarly, clearing a loan early helps you pay less in interest. Here is an example- If you borrow 10000 pounds for a year, 3 years and 5 years, your payments may look like this.

| Loan Term | Monthly Payment (£) | Total Payable (£) | Interest Cost (£) |

| 1 Year (12 months) | 865 | 10,380 | 380 |

| 3 Years (36 months) | 309 | 11,124 | 1,124 |

| 5 Years (60 months) | 198 | 11,880 | 1,880 |

- Step 6- Get the cash

Once you understand the terms and the repayments, provide your consent to the agreement. You may get the money in your bank account swiftly after that.

Later, you can set direct debits to pay automatically according to the payment schedule. It helps you remain on top of your payments without worries.

Bottom line

Thus, getting a loan of 1000-15000 pounds requires you to understand how the loan works. It helps you know whether the loan is right for you. Accordingly, you can decide the repayment potential by using the loan calculator. Compare loan costs and APR across providers through pre-qualification. It helps you fetch an affordable amount.

Jessica Rodz is the Senior Content Writer at Cashfacts. She has a long career in the field of content writing and editing. Jessica has the expertise in the UK lending marketplace where she has worked with 7 different lending organisations and acquired many responsibilities from preparing loan deals and writing blogs for their websites.

At Cashfacts, Jessica is managing a team of experienced loan experts and doing a major contribution in guiding the loan seekers via well-researched blogs. She has done graduation in Business (Finance) and now currently doing research papers on the UK financial sector.